Technical Article

The 48E Investment Tax Credit in the C&I Space

Introduction and Caveats

Tax credits for solar PV and battery energy storage project investments witnessed some stark revisions with the passing of H.B.1, the budget reconciliation bill, on July 4th. Paths forward remain for certain kinds of projects and tax filers in the commercial and industrial sector. Like all things Internal Revenue Code and policy, nuance and complexity require careful comprehension. Some caveats:

Caveat 1: Mayfield Renewables, Inc. and any educational materials we provide are not intended to be proper legal, tax, or financial counsel. Please consult with your tax attorneys regarding ITC eligibility and the particulars of your project.

Caveat 2: This article covers the investment tax credits section (ITC) 48E. While certain developments and projects might also consider production tax credits spelled out in section 45Y, any solar or solar+ energy storage facility cannot “double-dip” and claim the 48E credit for the same year or any earlier year, and another tax credit incentive under 45Y (or 45, 45J, 45Q, 45U, 48, 48A) of the Internal Revenue Code[1]. Also, the “Domestic Content Adders” that some projects might consider are still in play after H.B.1 and can be applied for in conjunction with 48E, but are not discussed below.

Let’s jump in.

1. On residential solar and storage assets: 25D phasing out, third-party ownership remains

Investment tax credits for homeowner-owned assets in the residential solar markets will be discontinued after the 2025 tax year. Any expenditures made after December 31st, 2025, will not be eligible for ITC. Importantly, per the new language in Section 25D, any “expenditures made” are explicitly understood as an expenditure “treated as made when the original installation of the item is completed” and usable.[2] A purchase order is not enough.

In short, the tax-filer of solar, storage, or solar+storage system investments must get the system fully installed by December 31st of 2025 to claim a 25D ITC. There are no safe harboring paths, similar to 48E paths described below.

While H.B.1 sunsets the ITC for homeowners who purchase these renewable assets with cash or loans (i.e. social-security-number-holding tax filers), third-party ownership (TPO) arrangements may continue to pursue 48E ITC (employer identification number tax filers). Some industry partners believe this abrupt sunsetting of 25D may encourage more TPO arrangements, such as subscriptions, leasing, and purchase power agreements in smaller-scale solar markets.'

2. “Safe harbor” to establish credit eligibility

Beyond this timeline, taxpayers have two safe harboring paths that must be documented and started before July 4th, 2026. The taxpayer seeking ITC must “commence construction” either via a) “physical works of significant nature” path or b) the ‘five percent test’ path. You don’t need to do both.

“Physical work of a significant nature” primarily refers to the construction and installation of components integral to the energy property's operation. It does not include work to produce components that are either in existing inventory or are usually held in inventory by a vendor. In addition, expenditures considered here do not include soft costs and preliminary activities to assess a resource or site, such as survey, permitting, designing, securing financing, engineering studies, and modeling.[2]

For the ‘five percent test’ path, the taxpayer must incur a minimum five percent of the total cost of the renewable energy assets by that safe harbor deadline of July 4, 2026. These summed costs are viewed on a depreciable basis and cannot include the land, nor any property “not integral” to the energy project itself.

Projects aiming to establish 48E eligibility will do so via safe harboring, with few exceptions (see 48E discussion below). Projects eligible under either safe harbor path have a four-year window from the beginning of construction to completion and installation of assets for service. This is known in the tax code as the “continuity requirement” for safe harboring. There are exceptions to the 4-year requirement, in the case of excusable delays outside the taxpayer’s control (weather, permitting bottlenecks, interconnection delays). Seek tax counsel for more details if you run into delays.

3. Executive order on safe harboring expected in August

These insights regarding safe harboring and the “commencing construction test” for 48E credit opportunities, especially, should be taken with a grain of salt. Following a July 7th executive order that looks to ensure that the "beginning of construction" requirements for tax credit eligibility are not circumvented, another executive order from the current administration to the US Treasury Department is expected around August 18th, roughly 45 days from the budget reconciliation’s signing.

Industry partners believe the executive order may change little regarding the timelines of safe harboring, as laid out above. Still, it may strengthen guidance to tighten enforcement on tax-filers establishing 48E eligibility via the “construction commencement” path.

4. C&I Energy Storage and Commercial-Scale Solar 48E ITC

The rules for claiming 48E for energy storage asset investment and solar asset investment differ:

For commercial storage. The 48E ITC for commercial storage received fewer revisions from H.B.1, and still matches the original IRA rules for projects that are safe harbored before July 6, 2026, can access a 30% 48E tax credit through tax year 2033, before the percentage of the credit begins to taper. This 30% can be prolonged longer should our national annual greenhouse gas emissions rate fall and stay below a threshold. Without that greenhouse gas emissions detail, conservatively speaking, the 48E credit percentages for storage will taper as follows: 30% credit through tax year 2033, 22.5% in 2034, 15% in 2035. Remember again that starting a storage project after tax year 2025 will also require the investment to meet the FEOC rules to claim 48E ITC.

For commercial solar. There are two separate ways to claim the 48E ITC for solar-only projects. You must either complete installation by the end of 2027 or establish eligibility via safe harbor before July 4th, 2026. With the safe harbor move, a demonstration of continuous progress is required if the construction and installation period extends more than four years. In both solar scenarios, a 100% eligibility to claim ITC requires meeting the FEOC rules if construction commences on or after January 1st, 2026.

For commercial solar+storage? Claiming 48E is possible for mixed investment into solar+storage projects. The tax-filer must document and establish eligibility separately and according to the separate material expenditure figures. When divvying, remember that only the hard costs of the solar and energy systems’ components and some shared components (conduit and conductors) count. Soft costs (permitting, engineering, modeling) will not be considered as part of the expenditure sum. This requires good-faith effort. Seek tax attorney counsel here.

5. Foreign Entities of Concern (FEOC)

Beginning next year, those seeking 48E investment tax credits for PV and energy storage investments will also need to meet specific foreign entity of concern (FEOC ) eligibility constraints. Any project construction commencing on or after January 1, 2026, will be ineligible for 48E credit if it is controlled by, owned by, or receives material assistance from a “prohibited foreign entity” (PFE). It bears repeating that any project that completes construction for tax purposes within the calendar year 2025 does NOT need to comply with the FEOC rules.

Furthermore, after commissioning, the ownership contact details matter as well. For a decade after a project is commissioned for service, ITC credits are subject to recapture. An expenditure under a contract or license that grants effective control to a PFE at any point in the 10 years after the project is placed in service could trigger full credit recapture.

Covered Nation: China, Russia, North Korea, and Iran. The Treasury’s Office of Foreign Assets Control names these four countries as “covered nations,” from which any energy project’s products, material assistance, and/or legal and financial influence must be limited. China is the most notable inclusion in the solar PV and battery energy storage markets and supply chains.

Specified Foreign Entities (SFE): These include a) entities controlled by companies incorporated in or with primary operation in a covered nation, b) any entity controlled by a covered nation citizen who is not a legal U.S. permanent resident, and c) other entitiy associations— governmental agencies from the covered nations, military companies from a covered nation operating in the USA, designated foreign terrorist organizations, individuals or operations with documented national security convictions,.

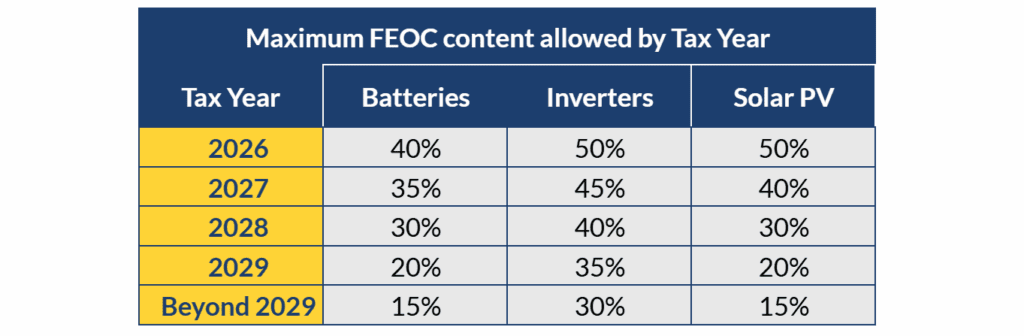

Material Assistance: HB-1 also prohibits projects from receiving “material assistance” from a PFE using the “material assistance cost ratio” (MACR). The MACR is calculated by subtracting the cost of PFE-sourced goods from the total cost of goods and dividing by the total cost of goods. Projects must meet specific MACR thresholds that vary by technology and construction year to remain eligible for credits.

Foreign Influenced Entities (FIE): Any specified foreign entity (SFE) has certain legal and financial control over an entity, such as the authority to appoint officers, maintaining 25+% ownership by a single SFE, maintaining 40+ % combined SFE ownership, ownership of at least 15% of the entity’s debt, or where an SFE receives certain payments from an entity that grants “effective control” to an SFE. “Effective control” includes agreements or arrangements that provide one or more contracted parties with specific authority over key aspects of the production of eligible components, energy generation, or energy storage, which are separate from any authority, ownership, or debt that would otherwise cause an entity to be an FIE.[3]

If the taxpayer fits SFE or FIE definitions in a tax year in which expenditures are made, those expenditures become ineligible for 48E credit. Also, a recapture of a 48E credit monies can happen anytime up to 10 years after construction completion, should asset ownership change to a “Prohibited Foreign Entity.”

6. Recap and Important Dates

Section 25D type tax credits for residential customer-owned PV, storage, and PV+storage assets will be discontinued after the 2025 tax year, with no safe harboring paths.

FEOC rules must be met for projects establishing 48E credit eligibility in 2026 or later. These rules include no financial affiliation with “Prohibited Foreign Entities” (such as “Specified Foreign Entities” and “Foreign Influenced Entities”) from China and three other covered nations. Repayment of 48E credit dollars may be required even 10 years post-construction, if asset ownership transfers to a "Prohibited Foreign Entity."

Safe harboring can be accomplished through the “physical works of significant nature” path or the ‘five percent test’ path. You don’t need to do both. In most scenarios, safe harbor must begin and be documented before July 6, 2026. The 48E energy storage credit rate schedule matches the 2022 IRA rules closely.

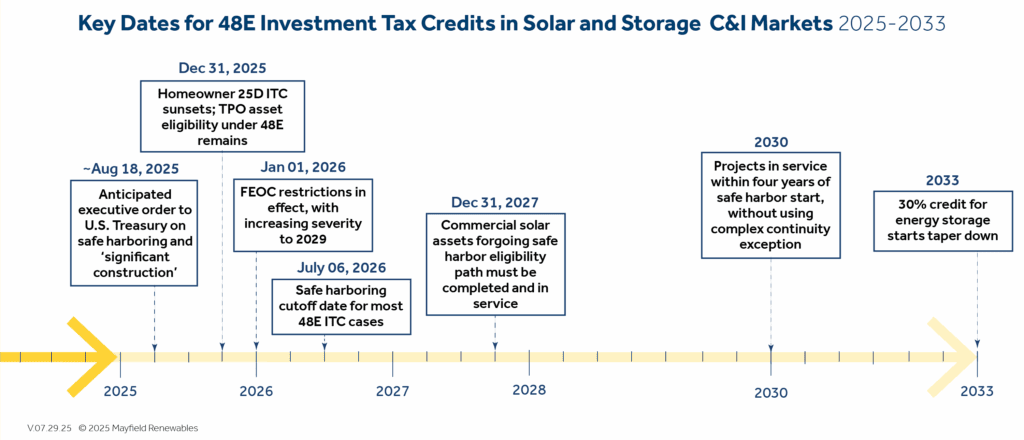

Here are the key dates to as we move forward:

1 The 45Y Clean Energy Production Credit After the Big Beautiful Bill

2 CALSSA-Member Webinar: “Credits in the Final Budget Reconciliation Bill”

Other Resources:

- House Bill 1 language

- Aurora Webinar (July 10): “OBBB: Solar Policy Updates Unpacked”

- SEIA on Commence Construction

- Foley on OBBB

‘Microgrid Economics and Financial Modeling’ is just one course offered at our Education Summit in October 2025. Mayfield Renewables also offers a library of courses to take at your own pace. If you're seeking design and engineering services for solar-plus-storage systems, contact us today for a consultation.